The Ad Agency Market Shift

Overview

This is Part II of a 3 part piece exploring the creative advertising market shift.

Part I debunks the myth that creative slowdown is caused by the economy.

Part II explores The Holding Company model and its role in gunking up creative.

Part III explores the limited leverage film production has in the pipeline, and what the industry should push for

Sections Below

A. Structural Issues - introduces the structural incentive issues of The Holding Company model, as well as where things stand today.

B. The Shift - The Creative Advertising Market Shift, and the 3 things creating it.

C. Operations & Disruptions - The operational issues of the model and their susceptibility to disruptions

High-Drama Quote

“The holding company concept was first introduced as a means of circumventing the longstanding industry norm that prohibits an advertising agency from serving competitors in the same market.

After finding that the major holding companies all realized positive scope economies…. large multi-brand advertisers seeking cost savings and other benefits.. consolidated their media buying across brands and markets with… those that are members of holding companies” The Unbundling of Advertising Agency Services (2010)

Structural Issues

Bundled Services

Having emphasized that there’s a disconnect between scope & budget in Part I, the question remains, why ad agencies are doing such a bad job bargaining for themselves.

It might be helpful to consider the overwhelming majority of Ad Agencies, are not actually bargaining for themselves, rather they are being bargained for, as part of a multi-part entrée. That is, these are agencies within Holding Companies, which comprise an overwhelmingly large fraction of the industry.

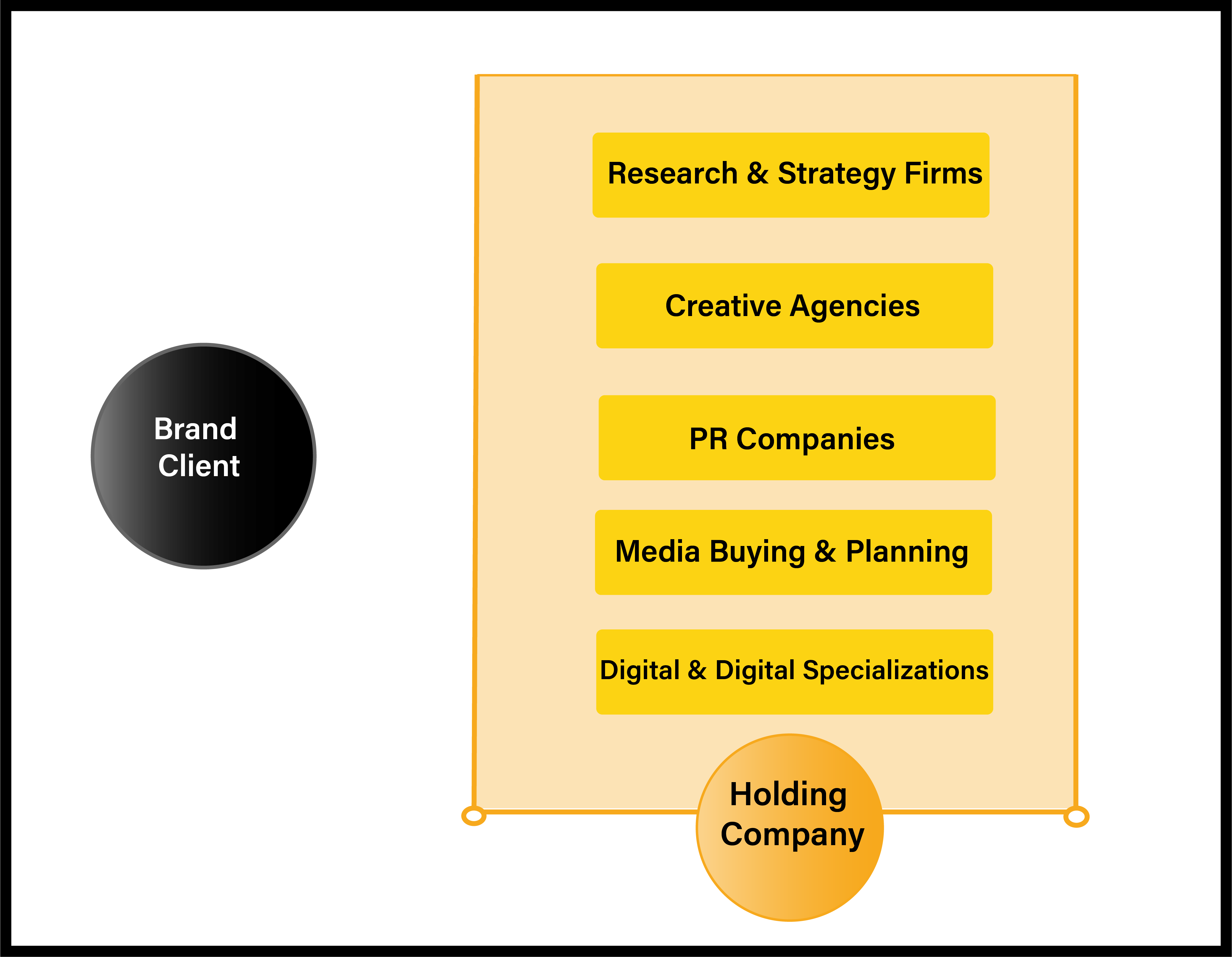

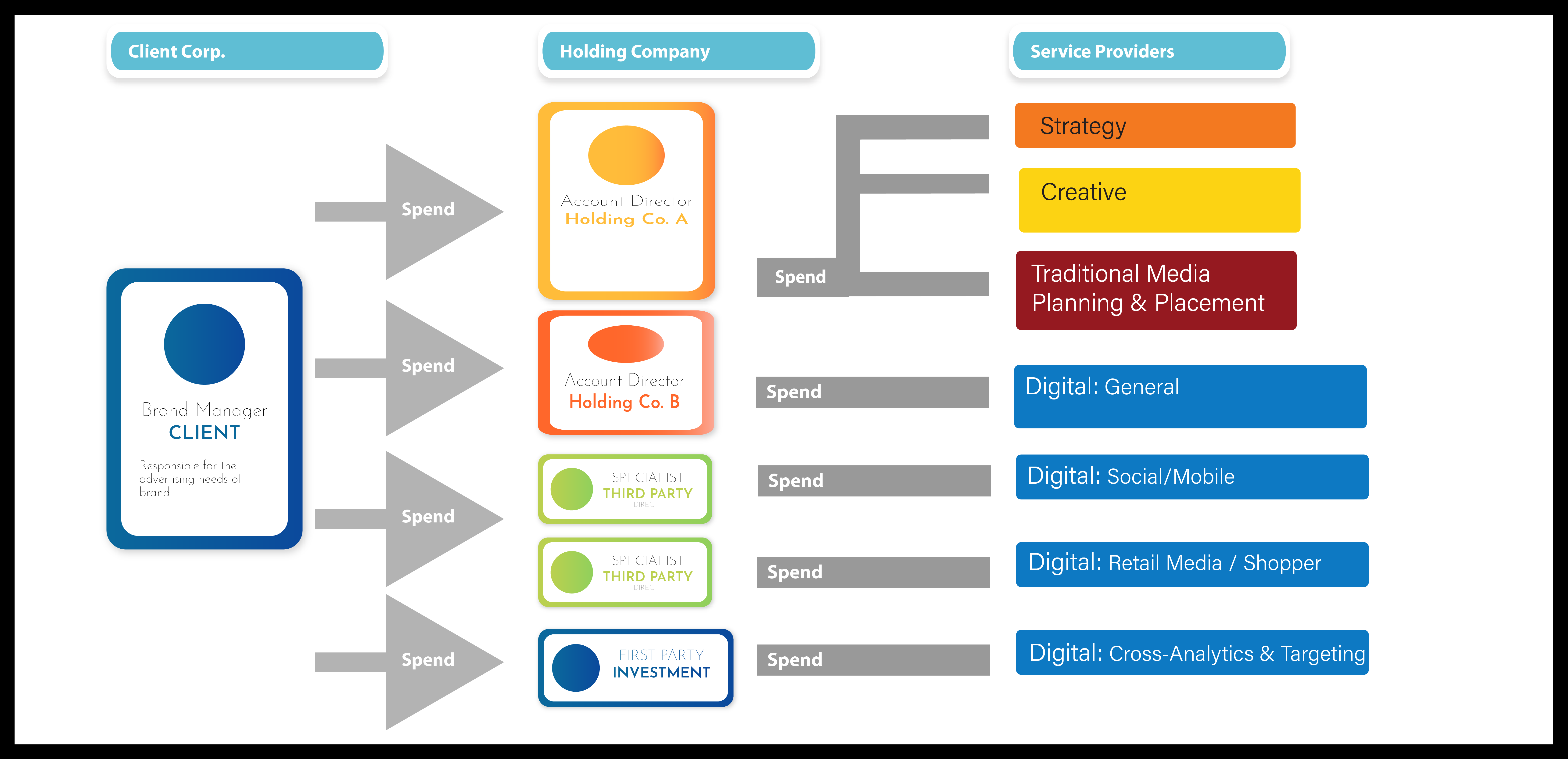

For those not familiar, an advertising holding company includes various agencies not just at the creative stage of the pipeline, but from end-to-end.

End to End Service Providers

End to End Service Providers

A holding company in its effort to capture a larger piece of the advertising pipeline, has a willingness to drive margins further down- than that in which an independent business owner would do.

When the independent business owner sits at the negotiating table, she needs consider the welfare of her business, employees, and overhead. At scale these things become flexible.

In a contagious interview, Michael Farmer, author of Madison Avenue Manslaughter stated

Agencies don’t have a pricing strategy for their work, and on 60% of their clients, they’re paid below what they need to be paid… that understaffing is the way they make their margins. And what a brilliant way to make the holding company happier: ‘Hey, we’re gonna make our numbers this year, we’re only stretching our people by an extra 40%,

Note on Terminology: Digital Media

In Part I I discussed the increased advertising spend, reflected in client annual reports, & industry reports, attributed to either Media or Digital Media. It may not be clear in the cases of individual reporting, but all of the following can fall under the umbrage of media.

- Traditional Media Planning and Buying: Creates strategic ad plans and purchases media across traditional channels like broadcast, print, and radio.

- Digital Agencies: Multi-channel digital strategies.

- Digital: Social Media: Targeted content creation and data-driven campaigns on social.

- Digital: Mobile: Strategies tailored to smartphones & tablets.

- Digital: Shopper: Targets shoppers with personalized strategies.

- Digital: Retail Media: Walled gardens, i.e. e-commerce platforms.

- Digital: Performance Analytics & Targeting: Sophisticated measuring, deciphering and tracking across modes.

Reports on increased media spend are seldom reflective of increased spend towards Traditional Media Buying and Planning services. Rather they reflect increases towards various digital fragmentations.

Incentive Streams

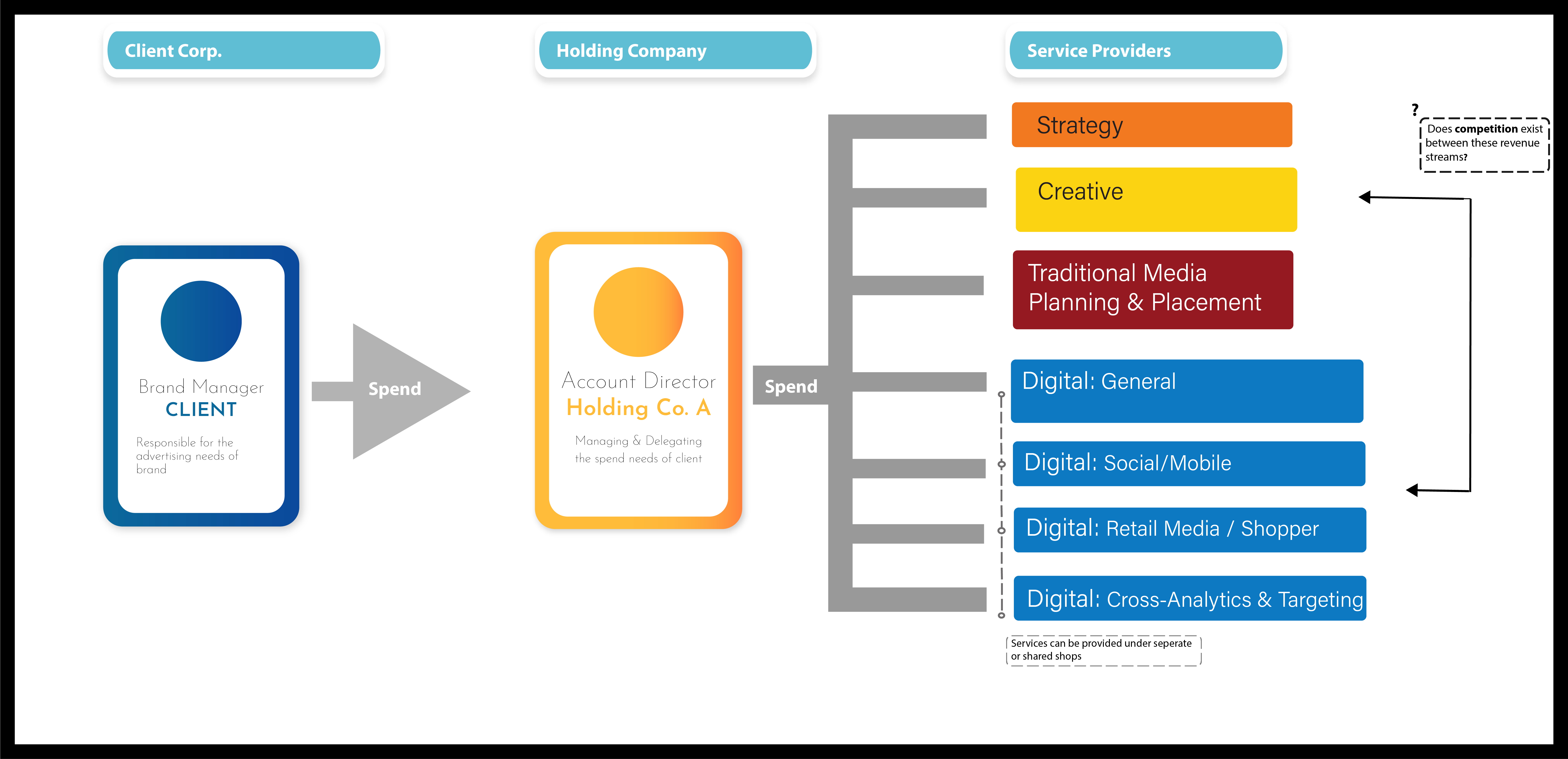

Considering the challenge The Holding Company has of managing different incentive streams, are there instances in which this becomes disadvantageous to a given stream?

For example if a brand wants to actively spend less on a creative shop, and more on a performance shop. If both shops are within the same holding company– is it a disadvantage for the creative shop?

See below

Diagram A: intra-competition

Diagram A: intra-competition

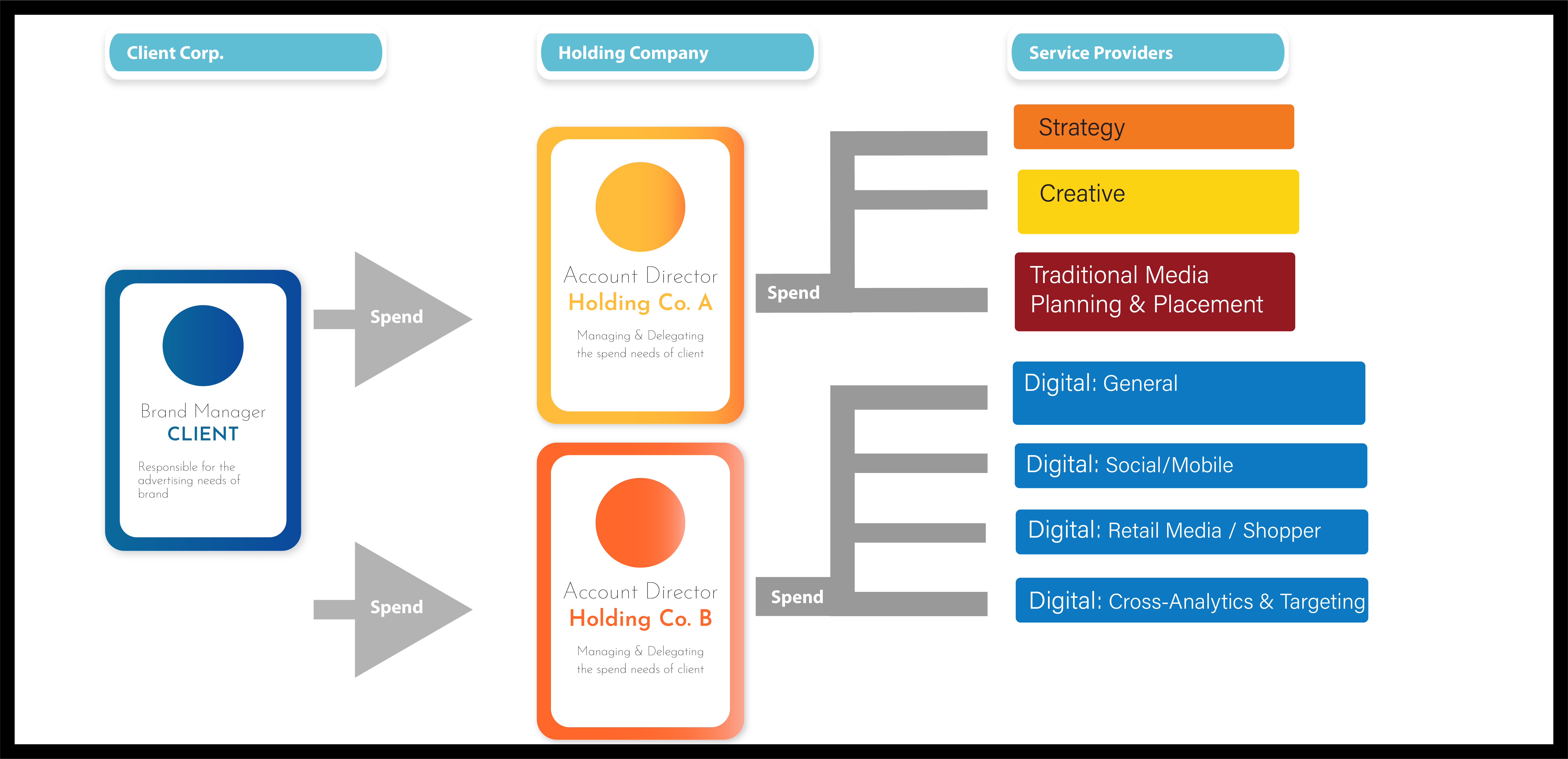

This may actually be a simplification though. What’s more realistic, is a Holding Company could be tasked with– being cognizant of client’s budget, and the various services it calls for, as well as how it integrates with other providers (which could even be a Holding Company)

Diagram B: complexity

Diagram B: complexity

In reality, the dynamic is very fragile. Although Holding Companies are tasked with managing providers that may be seeing increased spend, (in addition to those seeing decreased spend) those gains are meagerly covering their losses.

Holding companies are just barely holding onto profit. Smaller marketers have disrupted the space, and clients are investing heavily in first-party solutions. A given brand service pipeline might look more like this.

Diagram C: disruption

Diagram C: disruption

Where things stand

After going through the annual reports of each of the Big Six holding companies, a few consistencies in language stood out. Each report mentioned AI prioritizations in both generate and analytic AI. The creative sector was repeatedly noted as ‘resilient’ in the face of a soft market. Growth margins were thin, with Publicis leading at 6.3%, and Dentsu trailing at 1.6%. Restructuring and streamlining processes were common themes.

Also recent reporting, suggests an old habit of skimming large media buys nominal has reemerged. This isn’t actually reflective of industry disruption, rather its suggestive of Holding Company desperation to generate and hold onto extra cash.

Race to the Bottom

Consider the complexity of balancing intra-incentive streams of parallel & staggered companies alike. Consider the challenge of centralizing a diversity of companies into one framework. Consider all decisions and priorities trace back to a shareholder model, notorious for prioritizing short-term efforts of maximization over long-term wellbeing. This is how you create a race to the bottom.

There are corporate structures and governances that may work better here.

- A private entity would be afforded the wieldiness necessary to act in a way that protects its long term margins.

- A federation could provide a more decentralized approach, with a framework that actually does show resilience in the face of disruption.

- Even a publicly traded stakeholder model could offer marginal improvements, as opposed to the current shareholder model.

The Creative Advertising Market Shift

The culmination of 3 factors is creating the current work scarcity in the creative economy.

1. The Structural Issues of The Holding Companies - Bad incentive models as discussed above.

2. The Operational Issues of Agency-Client Pay Models - Discussed below. Operational issues only made possible by the structural issues above. Culminating as a disconnect between scope and budget.

3. Performance Media Drivers - This is where the disruption is coming from. Newly emergent drivers in the marketplace, and the growing call for “measurable” ad tech.

Operational Issues & Disruption

A Model that works for no one

Historic Context

Historically, agencies were paid on the basis of retainer fees, in recent decades this transitioned to capacity based pricing, the tracking of hourly billing.

This shift can partly be attributed to the never-ending appeasement of Brand Client procurement departments. It can likely also be attributed to conglomerate willingness to compete against one another on the margins.

Though imperfect, the retainer model incentivized agencies to view client relationships in a more long-term sense, promoting relationship building.

Pay Models Today

There’s been longstanding calls by various voices in the industry to change the way client compensation works. Although there are variances on a case by case basis, capacity based pricing, is largely the rule of thumb agencies live and die by. The issue with compensation, doesn’t just speak to pay, but also to how The Brand Client values creative.

Though capacity-based pricing is technically more favorable for the client in terms of marginal expense, it’s actually worse because it leads to–

- worse creative output by creative agency teams

- less creative alignment with strategy

- less generation of sales

- worse relationship building

- lesser client regard for creative, (irrespective of agency or success)

Expert Takes

Michael Farmer

Michael Farmer’s solution to this is simple. If sales performance is the client’s concern, than the client should pay and incentivize for performance. Pay for creative that solves problems. Farmer is in favor of a proprietary technique to value work and determine scope- called Scope Metric Units (SMU).

Blair Enns

Blair Enns author of Win Without Pitching, and Pricing Creative uses a framework that pits innovation and efficiency as opposites of the same spectrum. His feeling is that Holding Companies, acquire smaller companies to drive innovation. But in the act of acquisition, absorption and reorientation, said companies are pushed away from innovation and towards efficiency.

Blair: “The very culture of how they buy innovation destroys the innovation itself. It’s really helpful for the listener to understand and just to remember, you made the point earlier that at some point, like culturally, companies can’t innovate. They only acquire it, and the reason they can’t innovate is because this innoficiency principle is an issue of culture.”

Blair champions value-based pricing, in contrast to capacity-based and other hourly linked models, which he criticizes for their focus on time rather than client value.

Blair: “You and I have talked many times about the value of constraint-driven exercises, so if we’re trying to solve a problem and I impose a constraint on the problem, like time or money, et cetera, it’s entirely possible. In fact, I would say likely that in the right context, that constraint will actually trigger some breakthrough thinking on your end, and it will allow you to innovate. In one-off circumstances or situations, constraint-driven exercises can drive innovation, but a culture of constraints is an entirely different thing. A culture of constraints does not drive innovation at all. It has the opposite effect.”

Ariella Garcia

In a Forbes Video piece former executive Ariella Garcia, suggested that by clients ONLY paying for hourly labor, they in turn cause the agency to think ONLY in an hourly way.

- Rewarding only short-term results, leads to a greater likelihood employees will overlook long term issues. When confronted with the choice they will unconsciously favor just getting through the workday.

I pin this as being akin the Systems Thinking literature of Drift to Low Performance traps or Shifting the Burden traps

Robert Solomon

Robert Solomon pins the cost-cutting measures of Holding Companies, as to what’s driving the “growing unrest across agency-client relationships.” He attributes this as to causing a loss of institutional memory and relationship building.

Darren Woolley

Darren Wooley’s consultancy has suggested the solution to issues of scope is a combined format approach. One that more effectively link’s retainers to scope of work. By multiplying salary costs X overhead X profit margin.

The Point

The point here is not the respective operational issues and their fixes. But rather they are emerging in a larger environment of bad structural incentives.

Last year Ariella Garcia resigned her role as UM’s Worldwide Chief Privacy and Responsibility Officer , citing “incentive structures [as being ] fundamentally flawed and operating models that are inherently conflicted….She called out dysfunctional interdependencies, that serve no party effectively, not shareholders, not clients, and certainly not agencies.

Performance Media Disruption

The Structural Issues of The Holding Companies, have allowed for the creation of ineffective compensation models, which are now being exasperated by media disruption.

Without going into detail now, there is a push ‘away from branding’ and towards performance advertising happening. Ie, advertisement that can be measured and presented as justifiable ROI. A lot of the underlying logos imployed by tacticians here appeals towards fragmentation. Please note, I did not say this is happening “because of fragmentation”—rather, it’s because of appeals towards fragmentation.

I look forward to ten years from now, when the heavy spend on analytics is revealed to be largely a waste of money. Targeting has value, but there is a diminishing return.

More recent headlines have claimed a returned to branding based thinking, but there’s also been reporting that creative agencies themselves are pushing away from branding. Who doesn’t love the idea of WPP’s strategy to “build world-class, market-leading brands [through] AI data and technology”

If only Michael Crichton had written a book about Advertising, and not West World.

Moreover, my concern is that while the holding company networks are in the best position to advocate for the importance of creative work, they are also keen to capitalize on the newfound trend of performance-based spending.

{kind=link}